Red Flags Flashing: How the Strait of Hormuz Crisis Is Forcing Economists to Reassess the 2026 U.S. Outlook; And What It Means for Us as Investors

We’ve seen supply shocks before, but the current disruption in the Strait of Hormuz, effectively shut down amid ongoing military tensions with Iran, is delivering a double hit: slower growth potential paired with a sharp boost to inflation. For those of us managing portfolios through cycles, this is the moment to step back, separate noise from signal, and focus on durable fundamentals rather than short-term headlines.

The latest data paints a clear picture. Last week’s Producer Price Index (PPI) release already showed trouble: wholesale prices rose 0.7% in February with an annual gain of 4.3% (up from 2.8% in January). Core PPI, stripping out food and energy, climbed to 3.9% year-over-year — its highest level in more than a year. These figures don’t yet fully capture the post-February surge in crude oil, which is now working its way through the pipeline and into March readings and beyond.

Crude ended last week just below $100 per barrel, driving average U.S. gasoline prices above $3.90 per gallon (highest since September 2023, per AAA). While some relief appeared early this week, risks of prolonged disruption remain high. At the global level, the World Trade Organization warned that sustained elevated energy prices will slow world trade and economic activity more than previously expected, even as 2025 saw a boost from high-tech products that’s now easing.

The blockade is also hitting fertilizer supplies, raising concerns for agricultural producers and global food security. These are the kinds of second- and third-order effects that can linger and reshape cost structures across sectors.

Economists Are Adjusting, But Not Panicking

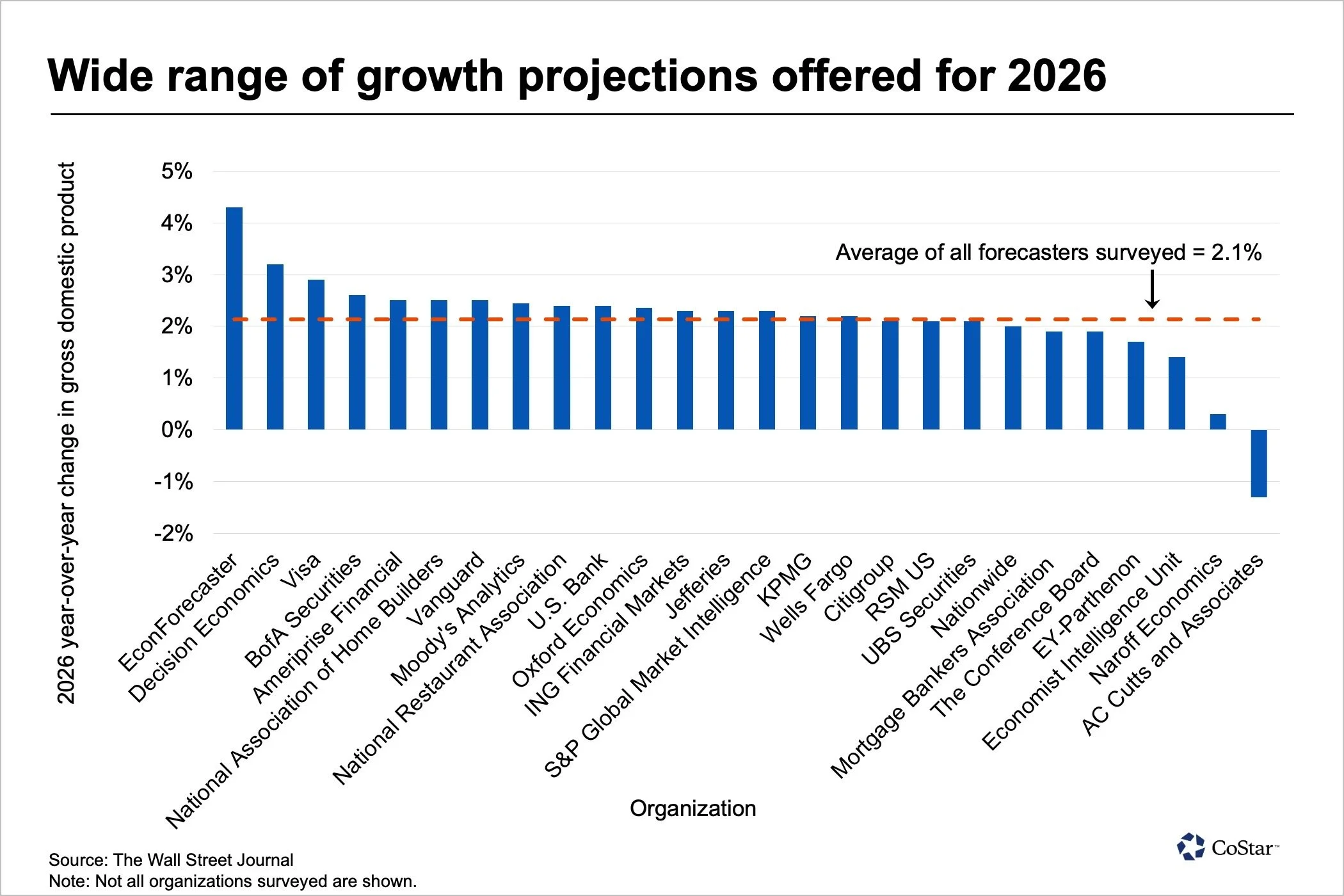

A mid-March Wall Street Journal survey of economists still paints a relatively sanguine baseline: any inflationary spike may prove temporary, with minimal long-term damage to growth or unemployment. Individual 2026 GDP forecasts ranged from a contraction of 1.3% to growth of 4.3%, averaging 2.1%, just a tick below the 2.2% average from the January survey taken before the conflict intensified.

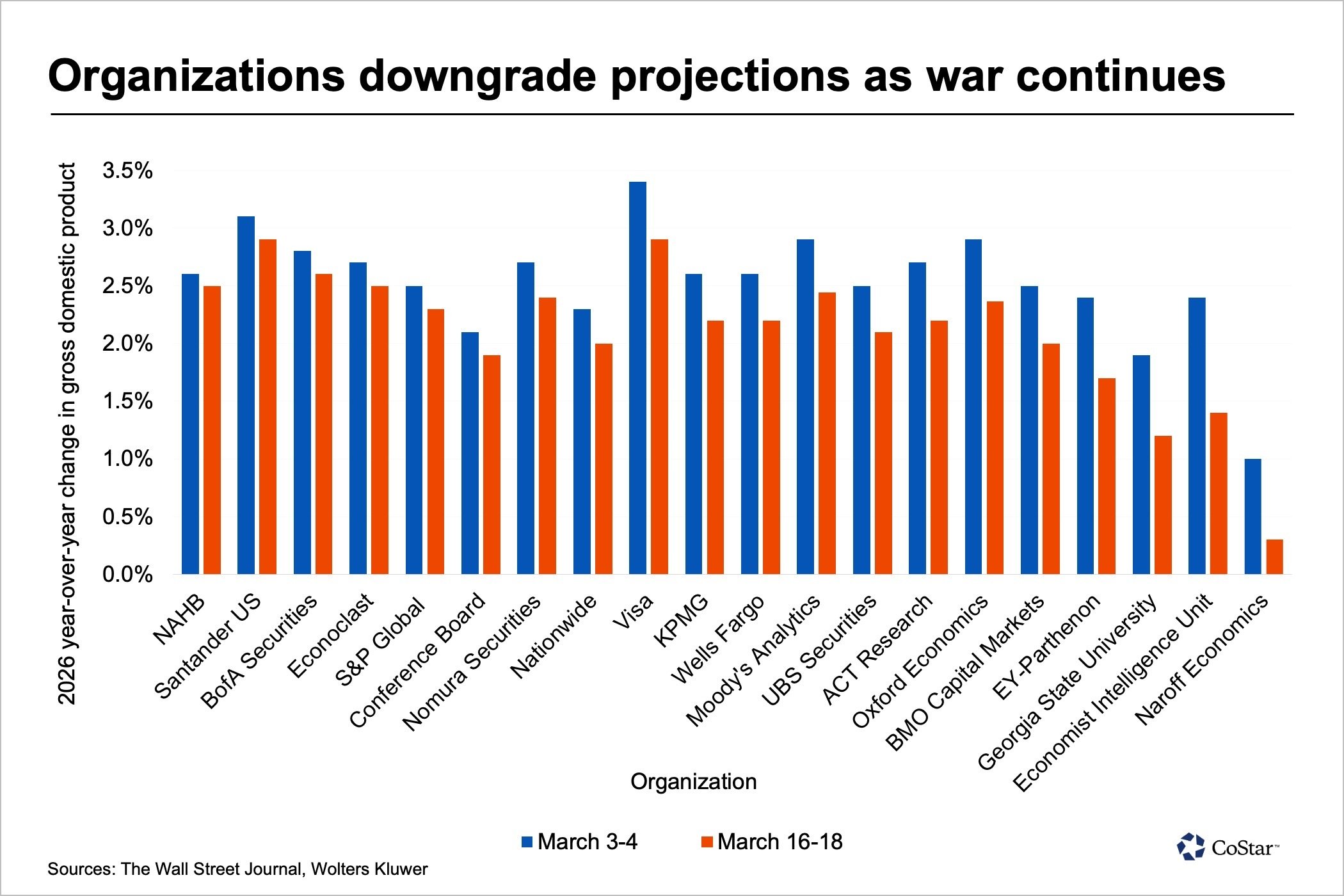

Yet the revisions are real. Professional forecasters have downgraded their 2026 growth estimates due to energy supply disruptions and uncertainty. In a follow-up comparison, respondents who answered both an early-March Wolters Kluwer survey and the later WSJ poll all lowered their numbers, with an average downgrade of 42 basis points.

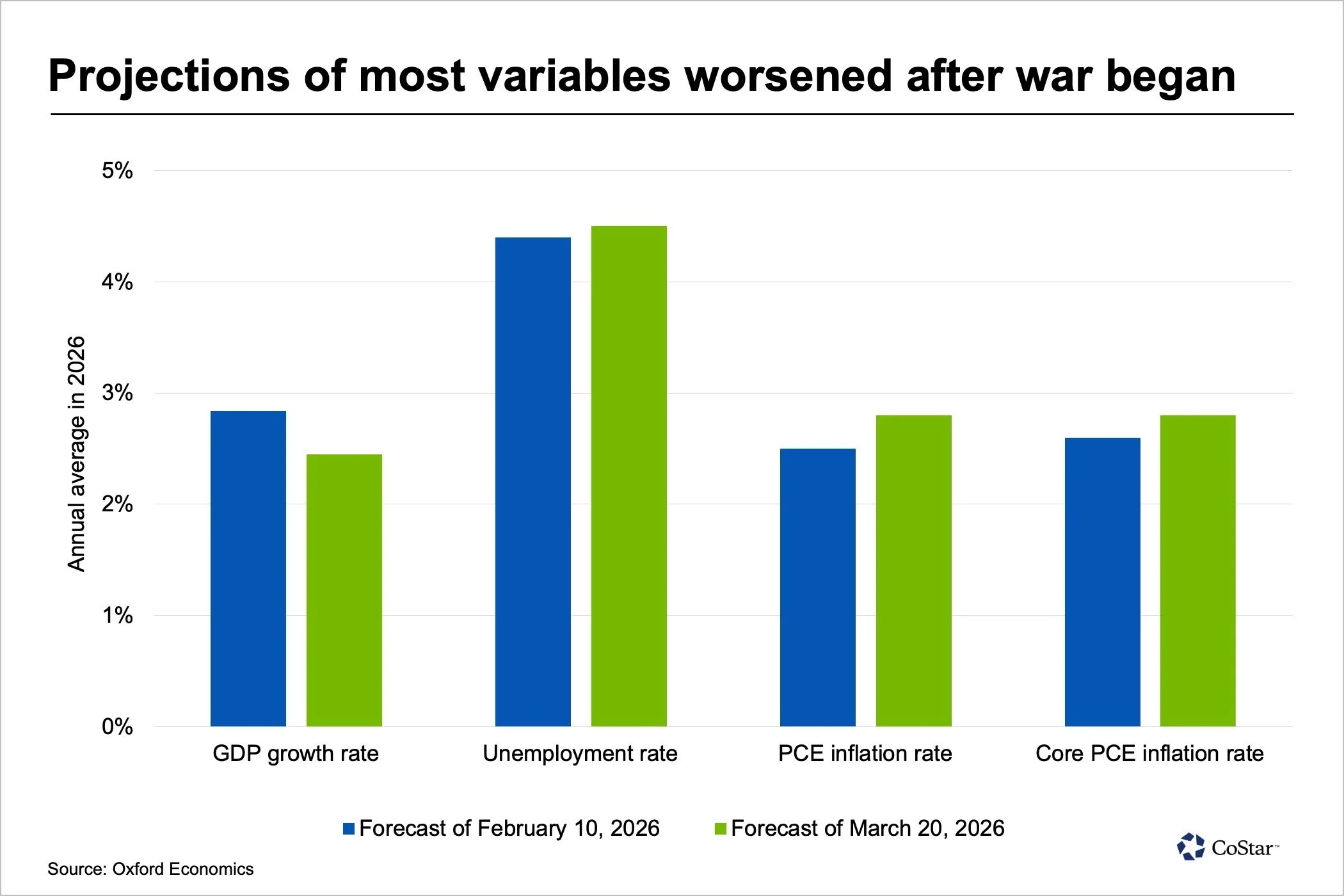

Oxford Economics, CoStar’s macroeconomic provider, recently revised its outlook downward. Instead of 2.8% growth in 2026 (driven by provisions in the One Big Beautiful Bill Act and regulatory reforms), they now project 2.5%. The firm attributes the change primarily to higher energy prices weighing on consumer and household spending, which accounts for roughly two-thirds of U.S. economic activity. In dollar terms, the expected fiscal boosts from the tax legislation are now seen as fully offset by elevated energy costs.

What We’re Watching Closely as Investors

This environment complicates the Federal Reserve’s dual mandate. A lingering inflation surge could push policymakers toward higher rates, yet the labor market is already showing signs of softening; with both job growth and labor supply slowing. Financial markets currently price in about a 35% probability of rate hikes by year-end, a sharp reversal from just weeks ago when cuts were widely expected and hikes were viewed as nearly impossible.

Key risks we track:

Persistent energy price pressure flowing into broader costs (transport, manufacturing, agriculture).

Weaker consumer spending as households absorb higher fuel and related expenses.

Fertilizer and food supply ripple effects that could add to inflation in unexpected ways.

Policy uncertainty around how many shocks the Fed feels it can “look through” before acting.

On the positive side, many economists still see the inflationary impact as largely supply-driven and potentially transitory if shipping lanes stabilize. The underlying U.S. economy retains strengths, including the tailwinds from the One Big Beautiful Bill Act on taxes and regulation, that could reassert themselves once the immediate shock fades.

How We Position Through Uncertainty

As experienced investors, we’ve navigated oil spikes, trade disruptions, and geopolitical events before. The playbook remains consistent: prioritize quality cash flows, maintain liquidity for opportunistic moves, diversify across resilient sectors, and avoid over-reacting to near-term volatility. Markets that digest supply shocks well often reward patience and disciplined allocation once the fog clears.

Periods like this test assumptions but also highlight the value of long-term alignment, whether in domestic growth corridors (like the Carolinas we’ve discussed), defensive real estate plays, or assets less sensitive to energy volatility.

If the evolving macro picture and its implications for your portfolio have you thinking about adjustments, I’d welcome a private conversation. No agenda, just a clear-eyed discussion grounded in the latest data and historical context.

👉 Schedule a private conversation here: https://www.johnnylynum.com/alignment

Disclaimer: This article is for informational and educational purposes only. It is not intended as financial, investment, tax, or legal advice. All data and forecasts referenced are based on public reports from the U.S. Bureau of Labor Statistics (PPI), Wall Street Journal economist surveys, Oxford Economics, AAA, and other sources as of mid-to-late March/early April 2026. Geopolitical events, energy markets, and economic conditions can change rapidly; actual outcomes may differ materially from projections. Past performance or trends do not guarantee future results. Individual circumstances vary; please consult your own qualified financial advisor, accountant, or attorney before making any investment decisions.