The Wealthiest Investors Don't Play the Same Game We Do

IMPORTANT DISCLOSURE — Please Read Before Proceeding

This article is intended for educational and informational purposes only and does not constitute personalized investment advice, a solicitation, or an offer to buy or sell any security or investment product.

All performance figures, return projections, and market data cited are drawn from publicly available third-party sources (Cambridge Associates, Preqin, JPMorgan Private Bank) and are presented for illustrative purposes only. Past performance is not indicative of future results. All investments involve risk, including the possible loss of principal.

Private equity and alternative investments are speculative, illiquid, and suitable only for investors who meet applicable suitability standards, including accredited investor status under SEC Regulation D. These investments are not FDIC-insured and are not bank deposits.

Any discussion of specific strategies, structures, or hypothetical examples is illustrative only and does not represent an actual offering. Before making any investment decision, consult with qualified financial, legal, and tax professionals regarding your individual circumstances.

For personalized advice aligned to your specific situation, schedule a one-on-one consultation at johnnylynum.com/alignment.

Private Equity Is No Longer Reserved for the Ultra-Rich. If You're Accredited, the Door Is Already Open.

I used to think private equity was a velvet-rope world. The kind of thing reserved for pension funds, endowments, and people whose last names are on buildings.

Then I got my accredited investor status and started paying attention to what was actually available, and what I found shifted how I thought about building long-term wealth entirely.

The institutions aren't putting 100% of their capital in public stocks. They're allocating meaningful chunks into private markets: private equity, private credit, real assets, venture. And for the first time in a meaningful way, accredited investors have access to the same table.

This article is the honest breakdown I wish I'd had earlier. The truth. Just what you need to know to decide if private equity belongs in your portfolio

Educational note: The above reflects a general market dynamic, not a guarantee of results. Access to private markets does not ensure outperformance. Individual outcomes vary significantly based on fund selection, timing, fees, and personal financial circumstances.

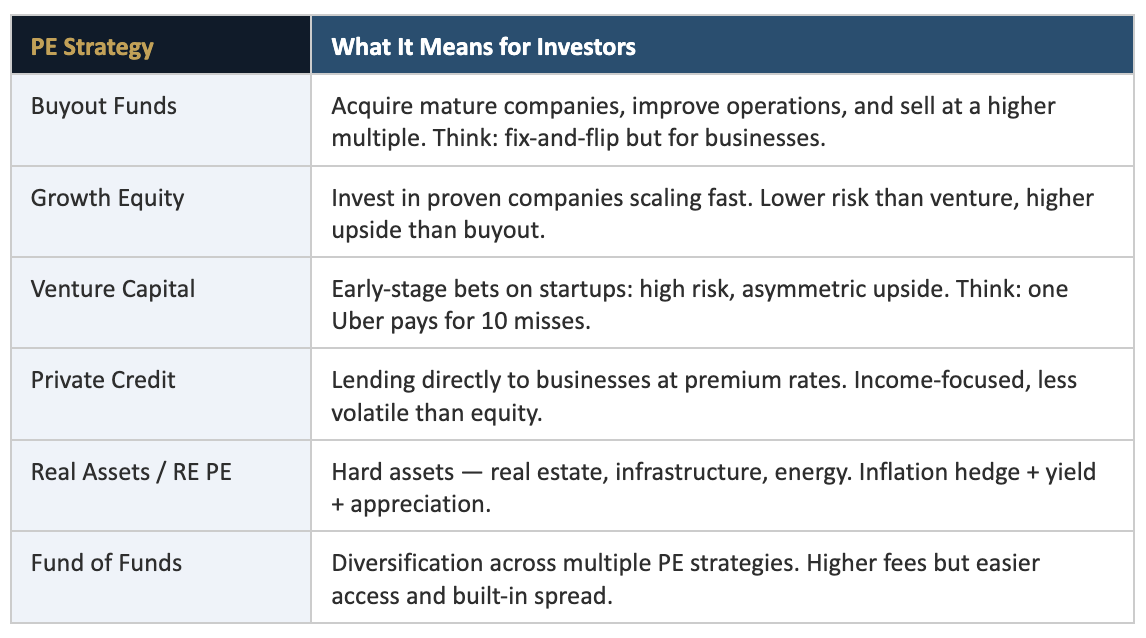

What Private Equity Actually Is (And What It Isn't)

Private equity is broadly defined as investing in companies or assets that are not publicly traded on a stock exchange. That's it. Everything else is detail.

But within that, the landscape is wide. Here's how we break it down:

Disclosure: The strategy descriptions above are generalizations for educational purposes. Actual fund structures, risk profiles, and return characteristics vary materially by manager, vintage year, and market conditions. Review each offering’s Private Placement Memorandum (PPM) before investing.

Each strategy carries different risk, return, and liquidity profiles. A sophisticated private equity allocation uses more than one.

The Numbers: Why Institutions Keep Going Back

Private Equity vs. Public Markets: The Long-Term Record

Let's talk about performance, because this is where the conversation usually starts and ends for most people.

According to Cambridge Associates data, private equity has outperformed the S&P 500 by an average of 3 to 5 percentage points annually over rolling 10- and 20-year periods. That spread compounds dramatically over time.

Performance disclosure: All return figures are sourced from third-party institutional research (Cambridge Associates, Preqin) and represent historical asset class averages, not specific fund or individual investor returns. Past performance is not indicative of future results. Target IRRs are projections only — they are not guaranteed and may not be achieved.

Yale's endowment, the gold standard in institutional investing, has consistently allocated 30–40% of its portfolio to private equity and venture. Their annualized returns have consistently outpaced the market over multi-decade periods.

That's not a coincidence. That's strategy.

The Illiquidity Premium: Getting Paid to Be Patient

Here's the honest trade-off: private equity is illiquid. When you invest in a fund, your capital is typically locked up for 5 to 10 years. You can't sell your position the way you can sell a stock on a Tuesday afternoon.

But that illiquidity is precisely why the returns are higher. You're being compensated for the one thing most investors refuse to do: be patient.

Liquidity risk: Investors in private equity funds should expect their capital to be illiquid for the duration of the fund’s life, typically 7–10 years. There is generally no secondary market guarantee. Early redemption, if available, may occur at a discount. Do not invest capital you may need access to before the fund’s expected term.

Who Qualifies: The Accredited Investor Standard

To access most private equity opportunities in the U.S., you must meet the SEC's definition of an accredited investor. As of 2026, that means:

Income exceeding $200,000 individually (or $300,000 with a spouse/partner) in each of the prior two years, with expectation of the same in the current year

Net worth exceeding $1,000,000, excluding the value of your primary residence

Certain professional certifications, including FINRA Series 7, 65, or 82 licenses

Knowledgeable employees of private funds also qualify under recent expansions

If you meet any of these criteria, you're already eligible. The question isn't whether you can access private equity; it's whether you're choosing to.

Regulatory note: Accredited investor status is a legal threshold established by the SEC. Meeting this definition does not mean that any specific investment is suitable for you. Suitability is a separate determination based on your individual financial situation, investment experience, risk tolerance, and goals. As a licensed financial advisor, Johnny Lynum conducts suitability assessments as part of any advisory engagement.

How We Evaluate Private Equity Opportunities

The 5-Question Framework We Use Before Writing Any Check

Not all private equity is created equal. Here's the honest filter we apply when evaluating any opportunity:

Who is the operator? Track record, alignment of interests, and skin in the game are non-negotiable. We want managers who co-invest their own capital alongside ours.

What is the thesis, and does the market support it? A compelling story needs a verifiable tailwind. We check independent data, not just the pitch deck.

What are the fee structures? The industry standard is 2% management fee and 20% carried interest. Deviations from this need a strong justification.

What's the liquidity structure and exit path? We want to understand how and when capital returns, not just the target IRR on paper.

What does the downside scenario look like? If the deal goes sideways, what do we own? Hard assets and secured debt create floors. Pure equity does not.

The Risks We Never Gloss Over

If you've made it this far, you deserve the honest part.

Private equity is not for everyone. Here are the risks we tell every investor before they commit capital:

Illiquidity risk: Your capital is locked up. Life changes. Emergencies happen. Never invest money you might need in the next 3–5 years.

Manager risk: The returns of private equity are highly manager-dependent. Top-quartile and bottom-quartile performance can differ by 10+ percentage points annually. Manager selection is everything.

Vintage year risk: Like wine, some years produce better returns than others. Deploying into a frothy market can compress returns. Timing matters, though it's never perfectly predictable.

Valuation opacity: Private assets don't have daily mark-to-market prices. This smooths volatility but also means you may not know exactly where you stand quarter-to-quarter.

Regulatory and tax complexity: K-1s, UBTI, state filing requirements. This is not a passive tax situation. Work with a CPA who understands alternative investments.

Risk disclosure: The risks listed above are not exhaustive. Additional risks specific to each fund or investment structure will be described in the applicable offering documents. Johnny Lynum, as a licensed financial advisor, discusses material risks with clients as part of any advisory engagement. This article does not substitute for that individualized discussion.

How to Start Building a Private Markets Allocation

The Simple Framework for First-Time PE Investors

You don't need to overhaul your portfolio overnight. Here's how we think about a rational, staged approach:

Start with investable assets: Test the waters with a single deal or fund. Learn the process, the reporting cadence, and the language. Don't overcommit before you understand what you own.

Diversify across vintages: Don't put all your PE capital into one fund that deploys in one year. Spread entry points across 2–3 years to reduce vintage risk.

Diversify across strategies: A mix of private credit (income), real estate (inflation hedge + yield), and growth equity (appreciation) creates a more resilient alternative sleeve.

Vet the operator obsessively: More than any other asset class, private equity returns come down to who is managing the capital. Reference checks, past fund performance, GP co-investment — these matter enormously.

Treat it as long-term capital: The investors who get hurt in private markets are the ones who needed the money before the fund wound down. Set expectations with yourself before you wire funds.

Allocation guidance disclosure: The allocation percentages referenced above reflect general industry guidelines from third-party sources and are not personalized investment recommendations. The appropriate allocation for any individual depends on their specific financial situation, risk tolerance, liquidity needs, tax circumstances, and investment goals. Consult with Johnny Lynum or another qualified financial advisor for a personalized assessment.

What We're Watching in Private Markets Through 2026–2028

The macro setup for private equity in the next 24–36 months is nuanced. Here's our honest read:

Private credit is having a moment: As banks pulled back from middle-market lending post-2022, non-bank lenders filled the gap at premium rates. Private credit AUM surpassed $1.7 trillion in 2025 and continues to grow.

Buyout activity is recovering: After a slow 2023–2024, deal flow picked up significantly in 2025 as rate expectations stabilized. Dry powder remains elevated, meaning capital needs to be deployed.

Real estate private equity is repricing: Similar to the Central Valley dynamic we described in our last piece, values corrected, cap rates reset, and opportunistic buyers are moving. The window is open.

AI and infrastructure themes are driving venture and growth equity: Energy infrastructure, data centers, and AI-adjacent businesses are attracting significant institutional capital with credible long-term theses.

Secondaries are emerging as a compelling entry point: Buying LP positions in existing funds at a discount gives investors an abbreviated J-curve and immediate diversification. Worth exploring.

Forward-looking statement disclosure: The market outlook above contains forward-looking statements based on current publicly available information and general market analysis. These are subject to significant uncertainty and should not be relied upon as predictions of future performance. Market conditions can change rapidly. All investment decisions should be based on current offering documents and current market information, in consultation with a qualified advisor.

This Is Where the Conversation Gets Personal

Everything in this article is general education. But here's the truth: the right strategy depends entirely on your capital position, your tax situation, your timeline, and your risk tolerance.

There is no one-size-fits-all answer. What works for a $500K portfolio looks different than what works for a $5M portfolio. And the only way to get to the right answer is to actually sit down and map it out.

If you're an accredited investor who's been wondering whether private equity belongs in your portfolio, or you're already involved and want a second opinion on how you're positioned, that's exactly the kind of conversation we have.

Just the facts, your choice of what to do next, and a focused conversation to see if there's alignment.

→ Secure Your Alignment Call

I keep a limited number of spots open each week for accredited investors who are serious about building wealth. If you want to walk through what this looks like for your specific situation, let's talk. johnnylynum.com/alignment

FULL REGULATORY DISCLOSURE

Author: Johnny Lynum is a licensed financial advisor. This article is published for educational and general informational purposes only. Nothing herein constitutes personalized investment advice, a recommendation to buy or sell any security, or a solicitation of any investment product.

Third-party data: All market statistics, performance figures, and allocation data cited are sourced from publicly available third-party research, including Cambridge Associates, Preqin, and JPMorgan Private Bank. Data is current as of the sources’ most recent publications as of early 2026.

Past performance: All historical return data and performance comparisons are for illustrative purposes only. Past performance of any asset class, index, or strategy is not indicative of future results.

Hypothetical examples: Any hypothetical investment examples, projections, or illustrations are for educational purposes only and do not represent actual funds, offerings, or investment results. Projected returns are not guaranteed.

Accredited investor status: Meeting the SEC’s accredited investor definition does not mean that any specific investment is suitable for you. Suitability requires an individual assessment of your financial situation, risk tolerance, investment experience, and goals.

No guarantee of results: All investments involve risk, including the possible loss of principal. Private equity and alternative investments involve additional risks, including illiquidity, leverage, and limited regulatory oversight.

Tax and legal: This article does not constitute tax or legal advice. Consult qualified tax counsel and legal advisors before making any investment decision.

Regulatory: Advisory services are subject to applicable federal and state securities laws and regulations. For a full description of services, fees, and disclosures, contact Johnny Lynum directly or visit johnnylynum.com.

© 2026 Johnny Lynum | All Rights Reserved | For Accredited Investors Only