The AI Infrastructure Boom Is the Biggest Capital Deployment Event of Our Lifetimes — and Most Investors Are Positioned for None of It.

$427M for a University Campus. $200B in Capex Planned for 2026. $700B Committed Across Big Tech.

When Amazon Buys a University, We Pay Attention

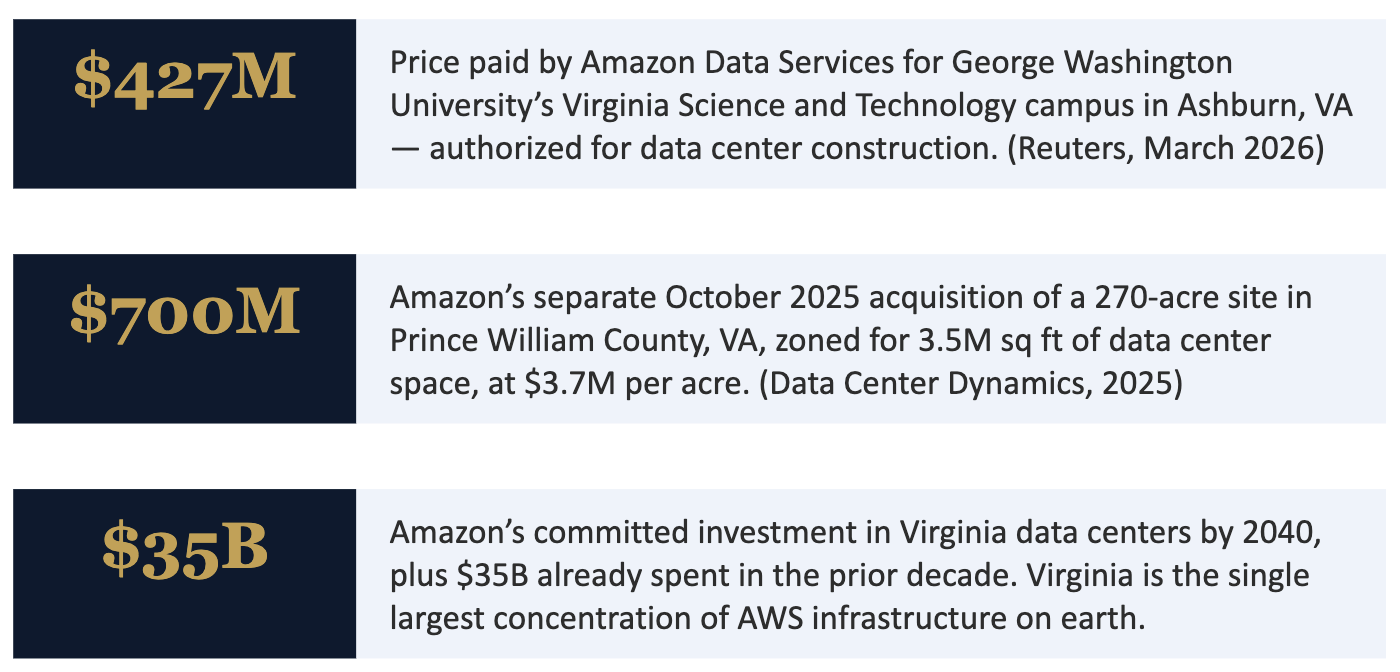

On March 2, 2026, Reuters broke the news: Amazon Data Services had acquired George Washington University’s Virginia Science and Technology campus in Ashburn, Virginia, for $427 million. The deed authorizes Amazon to build a data or information technology center on the site.

A university sold its campus to become a data center. That sentence alone tells you something about the scale and urgency of what’s happening in AI infrastructure right now.

GWU needed the capital. Amazon needed the land. And Ashburn, Virginia, already the data center capital of the world, just got denser. The university gets to keep programs at the site for up to five years, but the future of that land is already written: it will serve the AI economy.

What does this mean for investors? Quite a bit. Let’s break it down.

The Deal: What Actually Happened in Ashburn

The GWU campus acquisition is one piece of a much larger Amazon land and infrastructure buying spree across Virginia, but it’s a symbolically significant one.

Universities don’t sell campuses. Until they do. The fact that GWU, an institution facing structural deficits despite cutting jobs, executive salaries, and capital spending, found its best path forward was selling 125 acres of Northern Virginia real estate to Amazon is a signal about two things simultaneously: the financial pressure on traditional institutions, and the relentless demand pressure on AI infrastructure land.

In Northern Virginia alone, Amazon has committed to investing $35 billion in data centers by 2040, on top of $35 billion already spent in the decade prior to 2020. The GWU deal is the latest entry in that ledge, not the last.

This Isn’t One Deal. It’s a $700 Billion Infrastructure Sprint.

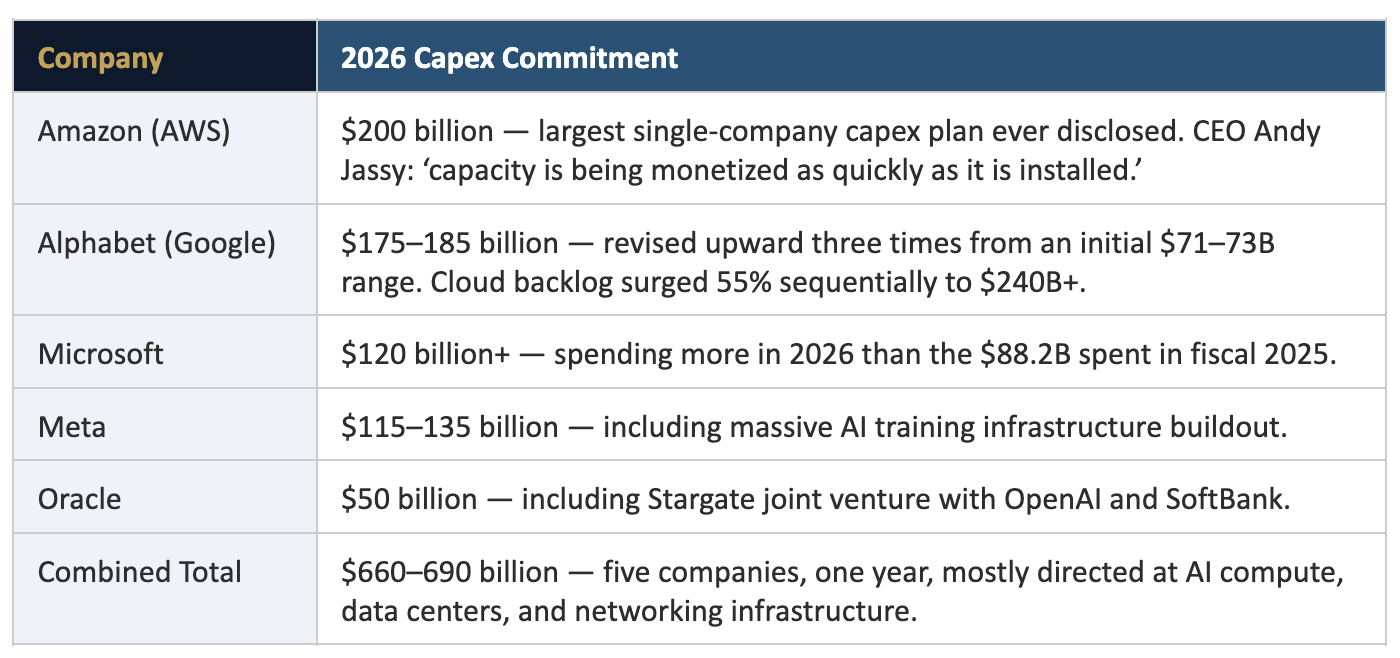

What the Hyperscalers Are Spending in 2026

The GWU acquisition is one transaction in one quarter of one company’s capital deployment plan. To understand the full investment thesis, you have to zoom out.

To put that in context: the entire U.S. interstate highway system cost approximately $500 billion in today’s dollars and took decades to build. These five companies are committing more than that in a single calendar year.

Amazon’s $200 billion figure alone caught Wall Street off guard — consensus expectations had been closer to $147 billion. The stock dropped 8–10% on the announcement. Investors are nervous about the payback period. But AWS CEO Andy Jassy’s counter: AWS hit a $142 billion annualized revenue run rate in 2025, with growth accelerating to 24% year-over-year, a three-year high.

The Demand Side: Why They’re Still Supply-Constrained

Here’s what makes this cycle different from prior tech bubbles: every major hyperscaler has publicly stated that their AI infrastructure business is supply-constrained, not demand-constrained.

Translation: they could sell more compute capacity than they can build. The bottleneck isn’t customers. It’s power, land, and construction timelines.

Goldman Sachs Research projects data center power demand to grow 50% to 92 gigawatts by 2027 — a 17% annual growth rate from 2025 through 2028

Data center occupancy rates are projected to climb from 85% in 2023 to over 95% by late 2026 — near full utilization

AWS alone added 3.8 gigawatts of new power capacity in the 12 months ending October 2025, effectively doubling its footprint since 2022

Deloitte estimates AI inference workloads made up half of all AI compute in 2025, rising to two-thirds in 2026 — driving sustained demand for always-on compute capacity

Why Virginia Keeps Winning; and What It Means for Real Estate

Ashburn, Virginia, is already the data center capital of the world. More internet traffic passes through Loudoun County than any other place on earth. Amazon’s acquisition of the GWU campus isn’t a bet on a new market; it’s a deepening of the most critical AI infrastructure hub in existence.

But Virginia’s data center boom is now radiating outward from Northern Virginia into Central Virginia, creating a cascade of investment that is reshaping the state’s economic geography:

EdgeCore Digital Infrastructure announced a $17 billion data center campus in Louisa County (June 2025)

CleanArc Data Centers announced a $3 billion campus in Caroline County (November 2025)

Google committed $3 billion in data centers in Chesterfield County, including 880 acres at Upper Magnolia Green and 350 acres at Watkins Centre South

Amazon’s Mattermeade project spans 1,143 acres across Caroline and Spotsylvania counties; 11 data center buildings targeting 770+ megawatts by 2027

Amazon’s separate October 2025 acquisition of the 270-acre Devlin Tech Park in Prince William County for $700 million, zoned for 3.5 million sq ft of data center space

For real estate investors, this creates a compounding dynamic: land near planned data center campuses appreciates. Power infrastructure follows. Workforce housing demand grows. The economic multiplier from a single large data center campus rivals that of a small manufacturing facility, with far less environmental footprint and far more sustained capital.

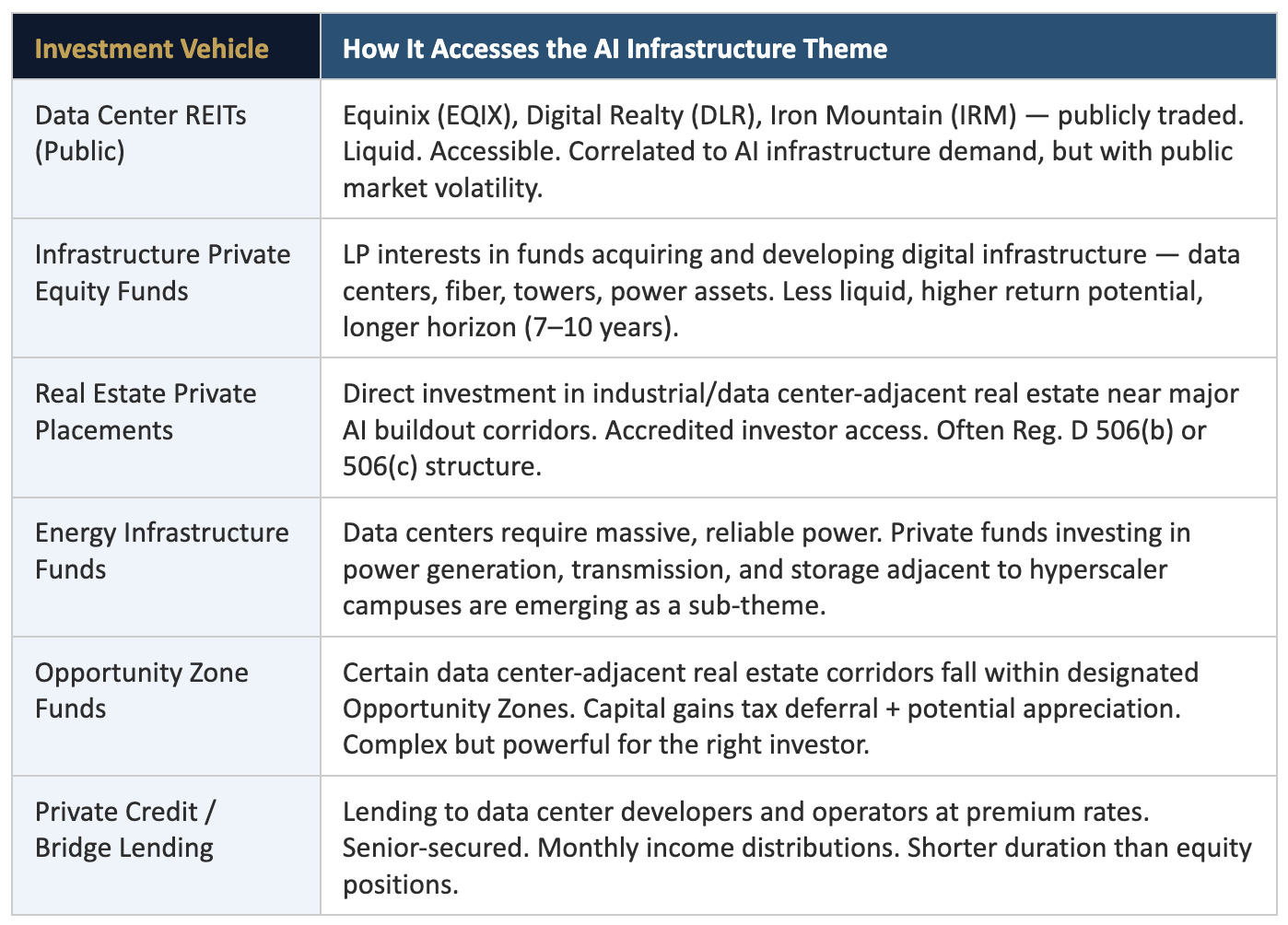

The Investor Angle: How Accredited Investors Access This Theme

You Can’t Buy Ashburn. But You Can Position Around It.

Let’s be honest: you’re not going to acquire land in Loudoun County and build a data center. That’s a hyperscaler game. But accredited investors have several legitimate paths to position themselves in the AI infrastructure buildout, from public REITs to private placements to infrastructure funds.

The Real Estate Angle Nobody Is Talking About

While most investors focus on the headline tech stocks, the infrastructure buildout is creating a quieter opportunity in commercial real estate: industrial, data center-adjacent, and workforce housing development near AI infrastructure corridors.

When a hyperscaler announces a major campus, it brings construction workers, permanent technical staff, and a service ecosystem. That economic activity needs to live somewhere; in housing, in retail, in industrial. The Central Virginia data center boom that we’ve been tracking is a direct investment thesis for multifamily and industrial real estate operators who understand the geography.

This is precisely the kind of asymmetric, non-obvious positioning that private placements and private equity funds can capture, before the broader market prices it in.

The Bear Case: What the Skeptics Are Saying

We don’t present one side of any trade without the other. Here’s what the skeptics — and there are credible ones — are concerned about:

The AI bubble question: Tech companies have collectively committed at least $630 billion in 2026 AI infrastructure. Some investors fear a growing AI-led bubble in which the pace of infrastructure investment outstrips the pace of monetizable AI application deployment. Amazon’s stock dropped 8–10% after its $200B capex announcement — reflecting genuine Wall Street skepticism about payback timelines.

Power constraints are real: The bottleneck for data center construction is not capital — it’s permitting for power transmission and the physical availability of electricity. 60% of industry professionals expect construction costs to rise 5–15% in 2026 as power and land competition intensifies.

Concentration risk in Virginia: Northern Virginia hosts a disproportionate share of global internet infrastructure. Regulatory changes, grid stress, or water supply issues could create systemic exposure.

Distressed sellers creating false signals: GWU sold its campus because it has a structural deficit. That’s a motivated seller, not necessarily a market signal. Investors should not mistake institutional distress for validated investment thesis.

AI revenue vs. infrastructure cost: OpenAI ended 2025 with approximately $20 billion in annual recurring revenue — a fraction of the hundreds of billions being spent on infrastructure on its behalf. The revenue-to-capex ratio remains deeply inverted.

This Is a Theme. The Question Is How You’re Sized.

Amazon buying a university campus for $427 million to build a data center is not a random real estate transaction. It’s a data point in the largest planned infrastructure deployment in American economic history. $660–690 billion in a single year. A data center in Ashburn. A 1,143-acre campus under construction in Central Virginia.

The AI infrastructure buildout is real. The revenue to justify it is still being demonstrated. That tension, between the certainty of the capital commitment and the uncertainty of the return timeline, is exactly the kind of environment where investor positioning matters.

If you’re an accredited investor and you want to think through how to access the data center, digital infrastructure, or AI-adjacent real estate themes through private placements, infrastructure funds, or other vehicles, that’s a conversation worth having now, before this becomes obvious to everyone.

Schedule Your Alignment Call → Johnny Lynum, Licensed Financial Advisor, Private Wealth Advisory

I keep a limited number of spots open each week for accredited investors who want a focused conversation about positioning in private markets, including the AI infrastructure theme. No pitch. No pressure. Just alignment. johnnylynum.com/alignment

Advisory services provided by Johnny Lynum, Licensed Financial Advisor. All engagements are subject to applicable suitability standards and regulatory requirements.