The Deals That Never Make the News Are Often the Best Ones

Private Placements Are Where Deals Get Done Before the Public Ever Hears About Them.

Here’s How Accredited Investors Get In.

Here’s something that rarely gets discussed in the mainstream financial media: every year, trillions of dollars in capital are raised through investments that never appear on a stock exchange, never get a Bloomberg headline, and are never available to the general public.

These are private placements; securities offered directly to a select group of qualified investors outside of the public markets. And if you’re an accredited investor, you have legal access to participate in them.

I’ve spent years watching investors with the same credentials sit in the same 60/40 portfolio while a completely different category of opportunity existed right beside them, never opened. That’s the gap this article is designed to close.

What follows is a practical, honest breakdown of what private placements are, how they’re structured, the regulatory landscape heading into 2026, and how we think about evaluating them.

*Educational note: The above is a general observation about private market dynamics, not a guarantee of returns or a description of any specific investment. Private placements involve significant risk and are not appropriate for all investors.

What a Private Placement Actually Is

A private placement is the sale of securities: equity, debt, or hybrid instruments — directly to a select group of investors without being registered with the SEC as a public offering.

Instead of an IPO or public bond offering, the issuer relies on exemptions under the Securities Act of 1933, most commonly Regulation D, to raise capital faster, with less disclosure, and at lower cost than a registered offering.

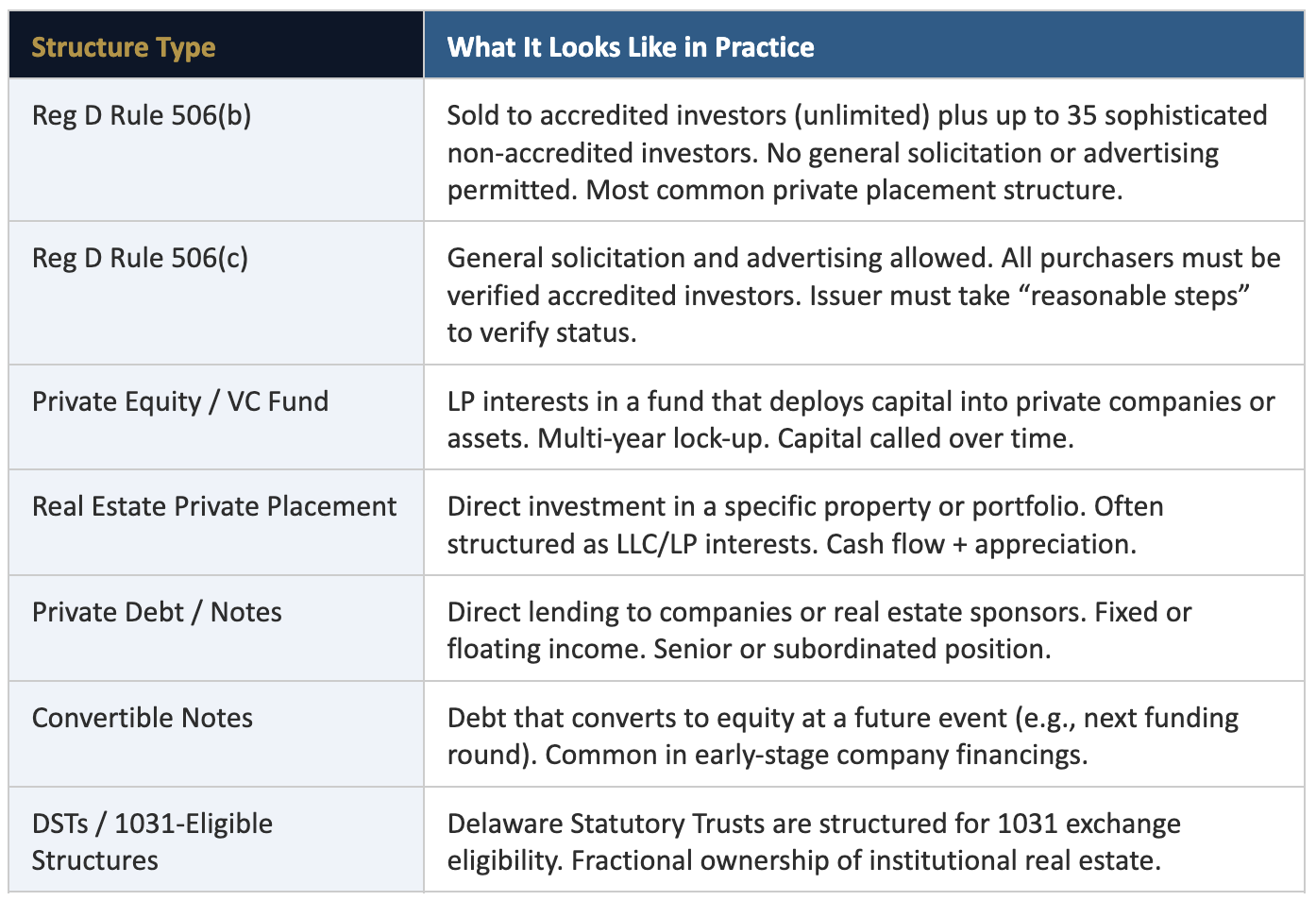

Private placements span an enormous range of structures and asset types:

*Regulatory note: The description of each structure above is a general summary for educational purposes only. Actual terms, rights, obligations, and regulatory requirements vary significantly by offering. Always review the Private Placement Memorandum (PPM), operating agreement, and subscription documents, and consult legal counsel before investing.

The Scale of the Private Placement Market Will Surprise You

How Much Capital Flows Through Private Placements Every Year

Most investors have no idea how large this market is because, by design, it operates largely outside public view.

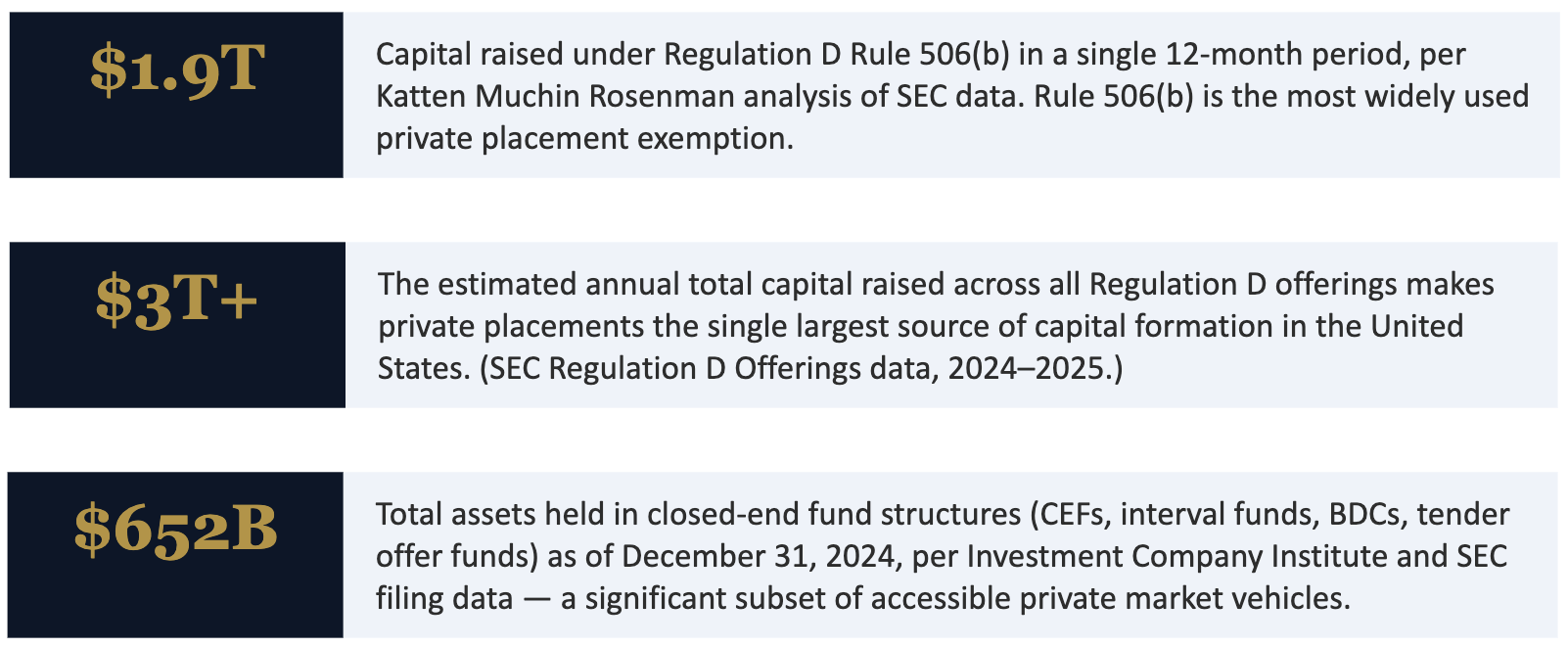

In a single recent 12-month period, issuers raised approximately $1.9 trillion under Rule 506(b) alone, the most widely used private placement exemption. Compare that to the roughly $124 billion raised under Rule 506(c) in the same period. Together, these numbers represent a private capital market that dwarfs most public market activity in any given year.

*Data disclosure: Capital market figures above are sourced from publicly available SEC data and third-party legal analysis (Katten Muchin Rosenman LLP, 2025). These are aggregate market statistics and do not represent returns to any specific investor. The private placement market is heterogeneous — individual deal outcomes vary widely.

This is not a niche, boutique corner of the financial system. Private placements are the primary mechanism through which American businesses and real estate operators raise growth capital. The question isn’t whether this market matters. The question is whether you’re participating in it.

The Regulatory Landscape in 2026: More Access Than Ever

What the SEC Has Changed — and Why It Matters for Accredited Investors

The regulatory environment for private placements shifted meaningfully in 2025 and is continuing to evolve in favor of broader access. Here’s what accredited investors need to know:

March 2025 — New SEC Guidance on Accredited Investor Verification (Rule 506(c)): The SEC staff issued a no-action letter and new Compliance and Disclosure Interpretations that significantly simplified the accredited investor verification process. An issuer may now reasonably verify accredited investor status by virtue of a minimum investment of $200,000 for a natural person, removing the historically burdensome requirement to collect tax returns and financial statements. This makes Rule 506(c) offerings more practical for both issuers and investors.

August 2025 — SEC ADI Update Opens Registered Funds to Private Markets: The SEC staff eliminated a longstanding informal position that required registered funds investing more than 15% of assets in private funds to limit offerings to accredited investors. This opens a new wave of accessible, registered fund structures that provide exposure to private markets for a broader investor base.

August 2025 Executive Order — Democratizing Access to Alternative Assets: President Trump signed an executive order directing the exploration of expanded access to alternative investments for 401(k) investors. While implementation details are still developing, the direction of policy is clear: the barriers between retail investors and private markets are being deliberately reduced.

2025 H.R. 3394 — Fair Investment Opportunities for Professional Experts Act: Introduced in Congress in May 2025, this legislation would expand accredited investor eligibility to include individuals with relevant professional expertise, regardless of income or net worth thresholds.

*Forward-looking regulatory note: The legislative and regulatory developments described above represent current proposals, guidance, and executive actions as of early 2026. Proposed legislation has not been enacted. Regulatory guidance is subject to change. Consult qualified legal counsel for current and applicable requirements before relying on any of the above for investment decisions.

Are You Accredited? The Current 2026 Definition

Under SEC Regulation D Rule 501(a), individual investors qualify as accredited investors if they meet any of the following criteria:

Income exceeding $200,000 individually (or $300,000 jointly with a spouse or spousal equivalent) in each of the prior two years, with reasonable expectation of the same in the current year

Net worth exceeding $1,000,000 individually or jointly with a spouse, excluding the value of the primary residence

Professional certifications held in good standing: FINRA Series 7 (General Securities Representative), Series 65 (Investment Adviser Representative), or Series 82 (Private Securities Offerings Representative)

Directors, executive officers, or general partners of the company selling the securities

Knowledgeable employees of a private fund (as defined under the Investment Company Act)

Family offices with assets under management exceeding $5 million, and family clients of qualifying family offices

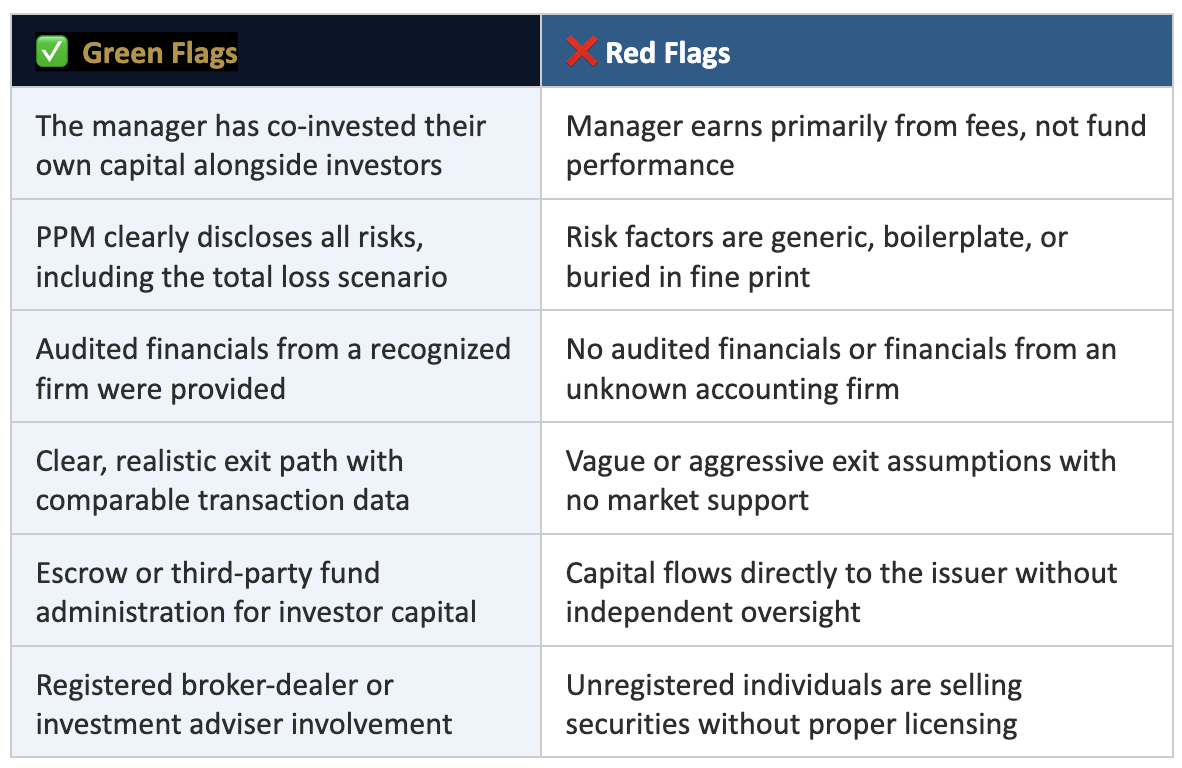

How We Evaluate Private Placements: The Honest Framework

What We Look at Before We Ever Tell a Client About an Opportunity

Private placements require more due diligence than public market investments — not less. The reduced disclosure requirements that make them efficient for issuers also mean investors must do their own homework. Here’s our process:

Step 1 — Read the PPM completely: The Private Placement Memorandum is the governing document. It contains the business plan, risk factors, use of proceeds, financial projections, management background, and legal terms. If you haven’t read it cover to cover, you haven’t evaluated the deal.

Step 2 — Verify the issuer and management independently: SEC EDGAR, state securities regulators, FINRA BrokerCheck, and basic business records are starting points. We check for prior enforcement actions, litigation, and background on key principals.

Step 3 — Evaluate the use of proceeds: Where is your money actually going? Operational capital, real asset acquisition, debt repayment, or management compensation? The waterfall matters.

Step 4 — Stress-test the return projections: Every PPM contains projections. We apply conservative assumptions to the downside case: higher vacancies, lower exit multiples, and delayed timelines. If the deal only works in the base case, it’s not a deal we recommend.

Step 5 — Understand the exit: Private placements are illiquid. We want to know the realistic path to return of capital: IPO, sale, refinancing, or cash flow distributions over time. If the exit is vague, that’s a red flag.

Step 6 — Review the fee structure and waterfall: Placement fees, management fees, carried interest, preferred returns, and promote structures all affect net investor returns. We model these explicitly.

*Due diligence disclosure: The process described above reflects general best practices in private placement evaluation. It does not guarantee investment performance or protection from loss. FINRA Rule 5123 requires broker-dealers to file private placement documents within 15 days of the first sale. Investors have the right to ask for and review all offering documents before committing capital.

What Good Looks Like vs. What Raises Flags

*Fraud awareness: The SEC and FINRA regularly issue investor alerts about fraudulent private placements, also known as “private placement fraud” or “Boiler Room” schemes. If an investment is being pitched with guaranteed returns, pressure to decide quickly, or resistance to providing documents, those are serious warning signs. Verify any offering on SEC EDGAR before investing.

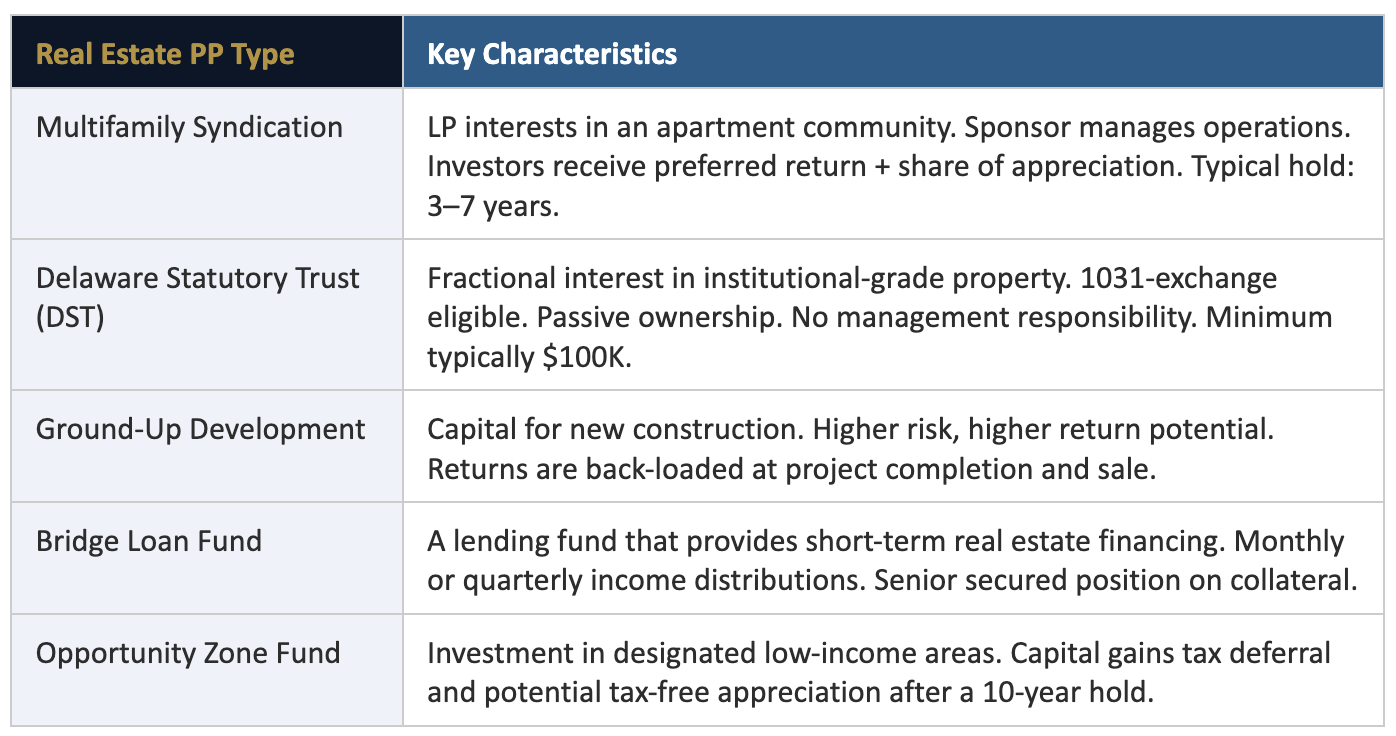

Private Placements in Real Estate: The Most Common Entry Point

For most accredited investors entering private placements for the first time, real estate is the most familiar and accessible on-ramp. Here’s how the most common structures work:

Real estate private placements have the advantage of tangible collateral — there’s a physical asset underlying the investment. That doesn’t eliminate risk, but it creates a floor that pure equity structures don’t have.

The tradeoff is illiquidity. A real estate syndication isn’t something you exit when the market moves. You commit, you hold, and you receive distributions according to the operating agreement.

*Real estate investment risk: Real estate values can decline. Rental income is not guaranteed. Private placements in real estate are illiquid and may be subject to market risk, interest rate risk, credit risk, and management risk. DSTs and Opportunity Zone investments carry additional regulatory complexity and tax considerations. Consult a CPA and legal counsel before investing.

What We’re Watching: Private Placement Trends into 2026–2027

The private placement market is not static. Several trends are actively reshaping who can access these investments, how they’re structured, and where institutional capital is deploying:

Democratization is accelerating: The combination of the March 2025 SEC verification guidance, the August 2025 ADI update, and the executive order on 401(k) access signals a sustained policy push to open private markets to a broader qualified investor base. This is the most significant regulatory shift in a decade.

Interval funds and tender offer funds are bridging the gap: With $99 billion and $80 billion in assets, respectively, as of year-end 2024, these registered fund structures provide quarterly or semi-annual liquidity windows while offering exposure to private market strategies. They’re increasingly used by accredited investors who want private market returns with more liquidity than a traditional LP fund.

Real estate private placements are repricing: As we covered in our Central Valley and broader PE articles, real estate values bottomed in 2024 and are recovering. Sponsors who raised equity at 2021 prices are returning capital and restarting fund cycles at reset entry points. New vintage opportunities are entering the market now.

Private credit placements remain a high-demand category: Direct lending, bridge loans, and preferred equity structures are absorbing significant investor demand as bank lending remains constrained in middle-market and commercial real estate. Yield-focused placements in the 9–12% range are attracting accredited investors seeking income.

AI and data infrastructure placements are emerging: Private placements in data centers, energy infrastructure, and AI-enabling businesses are attracting both institutional and accredited investor capital with credible long-term demand theses.

*Forward-looking statement: The trends described above reflect current market observations and publicly available regulatory information as of early 2026. Future developments may differ materially. All investment decisions should be based on current offering documents and consultation with qualified advisors.

The Private Placement Space Rewards the Prepared

Here’s the truth about private placements: they are not passive. They require you to understand what you’re buying, who you’re investing with, and what the realistic outcome range looks like, both good and bad.

The investors who do well here are the ones who take the time to understand the structure before they wire funds. The ones who get hurt are the ones who were attracted to a headline number without reading the underlying terms.

If you’re accredited and you’re starting to think seriously about private placements, whether real estate, private debt, or equity, the most valuable thing you can do right now is have a focused conversation to make sure you understand what you’re actually getting into.

That’s exactly the kind of work we do together before anything else happens.

→ Secure Your Alignment Call — Johnny Lynum, Licensed Financial Advisor

Private placements are one of the areas where having a licensed, accountable advisor in your corner matters most. I keep a limited number of spots open each week for accredited investors who are ready to do this the right way.

Advisory services provided by Johnny Lynum, Licensed Financial Advisor. All engagements are subject to applicable suitability standards and regulatory requirements.